- Complete integration with US intermediaries.

From Trump to Polymarket’s “hybrid” victory at TAR: the breakthrough of predictive betting in the World and in Italy [EXCLUSIVE]

![From Trump to Polymarket's "hybrid" victory at TAR: the breakthrough of predictive betting in the World and in Italy [EXCLUSIVE]](https://gambleanalytix.com/wp-content/uploads/2026/02/5e9baf0b2fe472df355f3a94d48a5ed6.jpg "From Trump to Polymarket's \"hybrid\" victory at TAR: the breakthrough of predictive betting in the World and in Italy [EXCLUSIVE]")

Kalshi is a fully regulated predictive contract exchange by the Commodity Futures Trading Commission (CFTC) in the United States, becoming one of the most important compliant infrastructure exchanges for institutional and retail traders.

Kalshi, Inc. is a US prediction market platform founded in 2018 by Tarek Mansour and Luana Lopes Lara, two former financial analysts who met at MIT (Massachusetts Institute of Technology). Today it is headquartered in New York City and is a private company with a market valuation of approximately $11 billion after a $1 billion funding round, with investors including Sequoia Capital, Paradigm, Y Combinator, and asset managers like Charles Schwab and Henry Kravis.

Kalshi is not a normal betting site: its offering is based on “event contracts”, financial contracts that allow users to buy/sell predictions on the outcome of real events — from climate and economic data, to politics, as well as sports and legislative results — with the contract price reflecting the market’s perceived probability. Unlike traditional bookmakers, Kalshi does not bet against the user but acts as an organized market where buyers and sellers meet, and it earns profits through transaction commissions.

The company operates as a regulated exchange in the United States under the authority of the Commodity Futures Trading Commission (CFTC), which in 2020 approved Kalshi as a Designated Contract Market — the first platform of its kind to obtain this federal recognition for predictive markets. This status allows it to offer tradable events, but it also entails legal challenges with individual states (especially when Kalshi began offering markets on sports results), because some state regulators believe that certain contracts constitute actual unauthorized sports betting.

In summary, Kalshi is seeking to redefine the boundary between predictive finance and regulated gaming, attracting both institutional liquidity and the attention of regulators, and positioning itself as a global market infrastructure for trading in advance on the outcome of real events.

![From Trump to Polymarket's "hybrid" victory at TAR: the breakthrough of predictive betting in the World and in Italy [EXCLUSIVE]](https://gambleanalytix.com/wp-content/uploads/2026/01/a53ab5d25285f39e081fb2f068694fd9.png)

The currency used by Kalshi ➡️ USD fiat — the main market is in US dollars.

Kalshi also allows deposits via stablecoins or cryptocurrencies in some cases, but these are automatically converted to USD before absorbing trading contracts.

Fiat currency means, from Latin, both made (by decree). When we talk about fiat currencies, we are talking about traditional currencies like the dollar, euro, yen, ruble, etc.

Key features:

👉 Although Kalshi may accept crypto deposits → USD, its core operation is tied to fiat currency markets, not native tokens or stablecoins as the primary market medium.

| Platform | Main Currency | Features | Typical User Type |

|---|---|---|---|

| Polymarket | USDC (stablecoin) | In transition, under CFTC compliance, decentralized structure | Global traders, crypto-native |

| Kalshi | USD (fiat) | CFTC regulated | Institutional / US retail traders |

| PredictIt | USD | It is a site focused on politics | Political bettors |

| Opinion.Trade | Crypto (e.g., BNB Chain token) | Decentralized | Crypto traders / dApp users |

| Crypto.com Markets | Crypto / stablecoin | Integrated exchange | Crypto Ecosystem |

✔️ The main prediction markets use a combination of currencies:

✔️ In the United States, it’s not that platforms have completely eliminated stablecoins, but Kalshi structures the use of cryptocurrencies as a gateway to convert them into fiat market, while Polymarket is trying to balance the use of stablecoins and regulatory compliance to fully re-enter the US market.

Within a few months, the advance of prediction markets (Kalshi, Polymarket, and the “event contracts” ecosystem) has forced the two giants of US betting — FanDuel (Flutter) and DraftKings — to make a choice: suffer competitors who bypass the state borders of traditional betting, or enter it with a proprietary product.

And the answer, today, is clear: they have entered it.

A stablecoin pegged to the dollar is, in essence, a digital dollar: a cryptocurrency designed to maintain a stable value (1 token = 1 USD) thanks to reserves in cash, government bonds, or liquid instruments held by the issuer. It is used to move money on the blockchain with the speed of crypto trading but with the stability of fiat currency, thus becoming the “cash” of digital markets, from payments to prediction markets. The most common are USDT (Tether), the queen for global volumes, USDC (Circle/Coinbase), perceived as more regulated and transparent in the US, and DAI, decentralized and collateralized on-chain. But their weight goes beyond finance: stablecoins have also become a geopolitical tool, as they effectively export the dollar outside the traditional banking system, allowing millions of people — and sometimes countries under sanctions or with weak currencies — to use “digital USD” without going through SWIFT or central banks. For Washington, it is monetary soft power; for regulators, it is also a systemic risk and a control issue: too many dollars circulating outside the banking perimeter mean fewer levers on capital, sanctions, and monetary policy. In short: fintech technology on the surface, but a struggle for economic sovereignty flows underneath.

The question on the minds of many keen observers is: “Are traditional bookmakers just watching while platforms operating (in most cases in markets not yet regulated) ‘eat up’ market share?”

In October 2025, the stock market crash of Flutter (owner of the leading US bookmaker Fanduel) and DraftKings sounded like an alarm bell.

Some stock market analysts were quick to draw a connection between the financial markets’ reaction and the new competition from Polymarket and its peers in sports.

There is also a significant detail, given that the decisive battle for the future of global betting is being fought in the USA (with substantial investments and strong “bets” and investments from Wall Street).

In important states (like California), betting is not legally permitted, but with the loophole of “financial” derivative contracts (recognized at the federal level), Polymarket and Kalshi are effectively collecting bets where no other betting operator is allowed. In the long run, this gap risks becoming insurmountable.

Other observers, however, attributed the causes to the negative results recorded by the house in the NFL (National Football League) in the last quarter, with many favored teams winning. Certainly, the unfavorable payout did not help the big players.

It’s difficult to give definitive answers, but one thing is certain: since then, the two main US bookmakers have announced that they are entering the predictive betting market with their own proprietary platforms.

FanDuel and DraftKings decided to move at that moment.

As I said, event contracts — framed as federally regulated derivatives/contracts — have allowed prediction markets to offer “bets” on sports and events even in states where online sports betting is not legal (California and Texas are among the wealthiest and most populous states). This has created a new competitive front and a jurisdiction war between federal regulation and state authorities.

Initially, prediction market platforms only offered binary options (yes or no, for example), but since 2025, they have introduced multiple options, including for sports, effectively becoming true betting platforms, but unregulated or operating in gray markets, thus having a competitive advantage.

When this step was taken, especially by financial exchanges — as I anticipated — Wall Street reacted negatively and also penalized stocks related to traditional betting, such as Flutter.

Precisely for this reason, the two main US bookmakers, Fanduel (owned by Flutter) and DraftKings, have adapted and are launching their own platforms.

FanDuel has not copied the Polymarket model: it has chosen a hyper-institutional path. At the end of December 2025, FanDuel and CME Group announced the launch of FanDuel Predicts, with an initial rollout in some states, under the umbrella of the federal financial derivatives oversight commission.

In the press release (and in the first public details), the approach is very clear: contracts on financial benchmarks (like stock indices and commodities) and economic indicators, in addition to the “event-based” perimeter. It is a way to:

When FanDuel decided to launch FanDuel Predicts, it didn’t just add a new feature to its app. It did something more subtle, and potentially more disruptive: it tried to shift the cultural boundary between betting and finance. For years, online betting has been presented as entertainment, adrenaline, cheering. Here, however, the grammar changes. You no longer bet on a match: you trade probabilities, buy scenarios, sell expectations. It’s the lexicon of markets, not betting slips. The collaboration with CME Group, the Chicago derivatives giant, is not a technical detail but a political manifesto: it means telling investors and regulators that these contracts resemble simplified futures more than bar bets. And indeed, the regulatory umbrella is not that of state gambling, but that of the federal Commodity Futures Trading Commission, the same authority that oversees commodities and financial markets. Inside FanDuel Predicts, you will find binary markets, yes or no, which can concern the outcome of a match but also the trend of the S&P 500, inflation, the price of oil. It is a silent mutation: the sportsbook becomes a small popular stock exchange, accessible from a smartphone, where the user is not just a fan but a micro-trader. And above all, it is a strategic move to circumvent the fragmented geography of US betting laws: where sports betting is still prohibited, federally regulated event contracts can still pass. Thus, FanDuel not only expands its offering but the very perimeter of the market, intercepting an audience that is not looking for stadium thrills, but for tools to monetize opinions about the world. If prediction markets truly become a new asset class, FanDuel Predicts is the signal that Wall Street and Las Vegas have stopped looking at each other with suspicion and have discreetly started talking to each other.

CME Group is a leading US global derivatives market company, operating major exchanges such as the Chicago Mercantile Exchange (CME), Chicago Board of Trade (CBOT), New York Mercantile Exchange (NYMEX), and COMEX. Through these platforms, it offers trading in futures and options on a wide range of assets — from interest rates and stock indices to currencies, commodities, and energy — enabling institutional investors and traders worldwide to manage risk, hedge positions, and access global benchmarks in financial markets.

DraftKings opted for the intermediary route with its own app. The well-known bookmaker officially entered prediction markets on December 19, 2025 with DraftKings Predictions, explaining that the operation is carried out through a subsidiary registered as an Introducing Broker and NFA member (National Futures Association), and is available in 38 states (including major markets).

For DraftKings, the value is twofold:

It is no coincidence that, as early as 2025, CEO Jason Robins openly spoke about the opportunity in “non-sports-betting states“.

Ultimately, setting aside the dust kicked up by tweets, stock market alarms, and regulatory anxieties, a rather American truth remains: prediction markets make a lot of noise, but little real damage. At least for now.

According to a report released by Citizens Equity Research, prediction markets have diverted about 5% of the regulated gaming volume from traditional bookmakers. Translated into dollars: about $8 billion per year. A figure that seems impressive only until you remember that the handle — the volume of bets — is not revenue, is not margin, is not profit. It’s movement. Like highway traffic: it doesn’t say how much the toll booth earns.

The analysis is signed by Jordan Bender, who immediately gets to the point: that 5% is slightly higher than previously estimated, but it is not an event capable of changing the fundamentals of the sector. No hemorrhage, no systemic business theft.

From the companies’ perspective, says Bender, the impact is a wash, a break-even. DraftKings, FanDuel (and therefore the parent company Flutter Entertainment) are not losing sleep: they are already present, directly or indirectly, in the world of prediction markets. If the game changes form, they change tables.

Some more trouble might come for those who have remained on the sidelines: Bet365, BetMGM, Caesars, Penn Entertainment. But even here, in the analyst’s words, we are talking about “slightly negative” scenarios. Nothing structural, nothing that justifies hysterics.

An exception is Rush Street Interactive: little exposure to prediction markets, excellent stock performance in the last year, and a strategy more focused on iGaming, which offers a certain immunity. On the contrary, paradoxically, the company could even benefit from the phenomenon: if yes/no markets erode the tax revenue from sports betting, they could push more US states to legalize traditional iGaming. The usual America: you lose on one side, you gain on the other.

But if companies manage, players do not. And this is where the story changes tone.

Data shows that retail users of prediction markets burn through money faster than any other form of gambling. In the first 90 days of entering these platforms, the average loss is 7% of bets, compared to 1% recorded in the rest of the online gambling ecosystem.

The reason is simple and cruel: in prediction markets, ordinary players do not compete against the house, but against other players, often much more prepared. “Sharp” bettors — those with models, official data, sophisticated pricing — find an ideal ground here, especially since platforms like Kalshi actively incentivize them.

The damage is amplified by another detail: the average bet. In prediction markets, it exceeds $185, more than triple the average of $55 in regulated sportsbooks. Losing more, more often, and with higher stakes is a lethal combination.

Bender synthesizes it without poetry but effectively: prediction markets are creating worse losses for the worst players, while the more skilled ones win more. Furthermore, the odds are generally worse than traditional bookmakers. Throughout the 2025 NFL season, for example, the prices offered by Kalshi consistently proved less favorable than those of DraftKings and FanDuel.

So why all this panic in the financial markets?

According to the analyst, because the reaction was disproportionate. DraftKings and Flutter stocks lost 33% and 30% respectively from their 52-week highs, but the real impact of prediction markets does not justify such cannibalization even remotely.

To be clear: a single bad Monday Night Football game can have a negative impact on EBITDA equal to — or greater than — everything that prediction markets are currently subtracting from the sector. And in the long run, Bender adds, the expansion of legalized online sports betting will tend to further restrict the space for these alternative markets, simply by offering a better product.

Finally, the map. Not all of America is the same. According to Juice Reel data, Florida, Georgia, and Texas remain on the sidelines of this phenomenon. Leading the way are the usual suspects: New York, New Jersey, California, Washington, and Ohio.

Prediction markets are not the end of bookmakers, nor the beginning of a new golden age. They are a noisy, fascinating, often ruthless experiment for the less equipped. And as always, in the great American casino, the real losers are not those who play the game, but those who think they have understood the rules without ever having read them thoroughly.

In summary:

One thing is evident happening on Wall Street: investors are desperately seeking listed companies that have a connection — even indirect — with this new segment.

The problem concerns the big names in prediction markets, such as Kalshi and Polymarket, which remain private companies. Conversely, some listed companies orbiting the theme, such as Robinhood Markets, are highly diversified financial groups, not platforms dedicated to trading predictive contracts.

The same applies to betting operators like DraftKings and Flutter Entertainment: they are now entering the world of prediction markets, but it is likely that, at least in the short term, this activity will represent only a marginal fraction of their revenues.

In the USA, there is one stock that has caught investors’ attention: High Roller, a company that manages online casinos in Scandinavian markets and is based in Malta.

Investors’ hunger for opportunities in this sector also explains the recent enthusiasm around the High Roller stock. It is not a “pure” prediction market company, but it is one of the few listed companies that allow investors to get close to that world.

When a new idea meets the market, it often happens like this: first euphoria, then selection. The price rises, falls, settles. And in the end, as always, only one question remains: how much of that promise will actually become revenue?

2026 has only completed one month, and the High Roller stock has already given its investors a rollercoaster experience. At the beginning of the year, the price hovered around $2. Then, in a matter of days, the surge: almost $24. Today, the value has halved.

A large part of that rally is concentrated on a single date, January 14, when the stock recorded an incredible +688 percent. That day, High Roller announced a partnership on prediction markets with Crypto.com. From that moment on, many traders began to look at the company not just as a simple online casino operator, but as a possible indirect bet on the world of event contracts.

“We are excited to bring High Roller to the United States through this strategic partnership with Crypto.com,” said CEO Seth Young. “Combining the huge appeal of prediction markets with our distribution capabilities is an extremely exciting opportunity.”

High Roller manages the online casino brands High Roller and Fruta and went public on Wall Street in October 2024, after reducing the size of its initial public offering just a month earlier.

How much of prediction markets will actually enter High Roller’s accounts, and with what margins? Today, no one knows, but the investors’ interest in these stocks remains tangible.

👉 Polymarket continues to operate with stablecoins (USDC) as the “base currency” for international predictive contracts.

Polymarket obtained, in November 2025, CFTC approval for a regulated return to the US market (U.S. Commodity Futures Trading Commission). It had blocked access to US users in 2022 after a regulatory action and a fine from the CFTC for operating as a derivatives market without registration.

✅ After three years, the CFTC issued an Amended Order of Designation allowing Polymarket to:

Why this step is important

🔹 The approval allows Polymarket to operate under the same regulatory framework as US exchanges (at the federal level, but we will see the problems encountered in individual states)

🔹 US users will be able to access prediction markets through regulated channels (no longer just offshore).

🔹 The platform has already enhanced its compliance, supervision, clearing, and regulatory reporting systems to meet the required standards.

How it got there

➡️ Polymarket acquired QCX LLC, a CFTC-licensed derivatives exchange and clearinghouse, thus providing the legal basis to operate in the US market.

Broader implications

👉 The move signals greater regulatory acceptance of prediction markets in the USA (undoubtedly Trump’s election facilitated this process).

👉 Potential increase in trading volume in the sector compared to the previous situation.

👉 Polymarket’s return contributes to pushing prediction markets into the traditional financial ecosystem.

Next steps

⏳ Before regulated trading becomes fully active, Polymarket must:

Kalshi is a fully regulated predictive contract exchange by the Commodity Futures Trading Commission (CFTC) in the United States, becoming one of the most important compliant infrastructure exchanges for institutional and retail traders.

Kalshi, Inc. is a US prediction market platform founded in 2018 by Tarek Mansour and Luana Lopes Lara, two former financial analysts who met at MIT (Massachusetts Institute of Technology). Today it is headquartered in New York City and is a private company with a market valuation of approximately $11 billion after a $1 billion funding round, with investors including Sequoia Capital, Paradigm, Y Combinator, and asset managers like Charles Schwab and Henry Kravis.

Kalshi is not a normal betting site: its offering is based on “event contracts”, financial contracts that allow users to buy/sell predictions on the outcome of real events — from climate and economic data, to politics, as well as sports and legislative results — with the contract price reflecting the market’s perceived probability. Unlike traditional bookmakers, Kalshi does not bet against the user but acts as an organized market where buyers and sellers meet, and it earns profits through transaction commissions.

The company operates as a regulated exchange in the United States under the authority of the Commodity Futures Trading Commission (CFTC), which in 2020 approved Kalshi as a Designated Contract Market — the first platform of its kind to obtain this federal recognition for predictive markets. This status allows it to offer tradable events, but it also entails legal challenges with individual states (especially when Kalshi began offering markets on sports results), because some state regulators believe that certain contracts constitute actual unauthorized sports betting.

In summary, Kalshi is seeking to redefine the boundary between predictive finance and regulated gaming, attracting both institutional liquidity and the attention of regulators, and positioning itself as a global market infrastructure for trading in advance on the outcome of real events.

The currency used by Kalshi ➡️ USD fiat — the main market is in US dollars.

Kalshi also allows deposits via stablecoins or cryptocurrencies in some cases, but these are automatically converted to USD before absorbing trading contracts.

Fiat currency means, from Latin, both made (by decree). When we talk about fiat currencies, we are talking about traditional currencies like the dollar, euro, yen, ruble, etc.

Key features:

👉 Although Kalshi may accept crypto deposits → USD, its core operation is tied to fiat currency markets, not native tokens or stablecoins as the primary market medium.

| Platform | Main Currency | Features | Typical User Type |

|---|---|---|---|

| Polymarket | USDC (stablecoin) | In transition, under CFTC compliance, decentralized structure | Global traders, crypto-native |

| Kalshi | USD (fiat) | CFTC regulated | Institutional / US retail traders |

| PredictIt | USD | It is a site focused on politics | Political bettors |

| Opinion.Trade | Crypto (e.g., BNB Chain token) | Decentralized | Crypto traders / dApp users |

| Crypto.com Markets | Crypto / stablecoin | Integrated exchange | Crypto Ecosystem |

✔️ The main prediction markets use a combination of currencies:

✔️ In the United States, it’s not that platforms have completely eliminated stablecoins, but Kalshi structures the use of cryptocurrencies as a gateway to convert them into fiat market, while Polymarket is trying to balance the use of stablecoins and regulatory compliance to fully re-enter the US market.

Within a few months, the advance of prediction markets (Kalshi, Polymarket, and the “event contracts” ecosystem) has forced the two giants of US betting — FanDuel (Flutter) and DraftKings — to make a choice: suffer competitors who bypass the state borders of traditional betting, or enter it with a proprietary product.

And the answer, today, is clear: they have entered it.

A stablecoin pegged to the dollar is, in essence, a digital dollar: a cryptocurrency designed to maintain a stable value (1 token = 1 USD) thanks to reserves in cash, government bonds, or liquid instruments held by the issuer. It is used to move money on the blockchain with the speed of crypto trading but with the stability of fiat currency, thus becoming the “cash” of digital markets, from payments to prediction markets. The most common are USDT (Tether), the queen for global volumes, USDC (Circle/Coinbase), perceived as more regulated and transparent in the US, and DAI, decentralized and collateralized on-chain. But their weight goes beyond finance: stablecoins have also become a geopolitical tool, as they effectively export the dollar outside the traditional banking system, allowing millions of people — and sometimes countries under sanctions or with weak currencies — to use “digital USD” without going through SWIFT or central banks. For Washington, it is monetary soft power; for regulators, it is also a systemic risk and a control issue: too many dollars circulating outside the banking perimeter mean fewer levers on capital, sanctions, and monetary policy. In short: fintech technology on the surface, but a struggle for economic sovereignty flows underneath.

The question on the minds of many keen observers is: “Are traditional bookmakers just watching while platforms operating (in most cases in markets not yet regulated) ‘eat up’ market share?”

In October 2025, the stock market crash of Flutter (owner of the leading US bookmaker Fanduel) and DraftKings sounded like an alarm bell.

Some stock market analysts were quick to draw a connection between the financial markets’ reaction and the new competition from Polymarket and its peers in sports.

There is also a significant detail, given that the decisive battle for the future of global betting is being fought in the USA (with substantial investments and strong “bets” and investments from Wall Street).

In important states (like California), betting is not legally permitted, but with the loophole of “financial” derivative contracts (recognized at the federal level), Polymarket and Kalshi are effectively collecting bets where no other betting operator is allowed. In the long run, this gap risks becoming insurmountable.

Other observers, however, attributed the causes to the negative results recorded by the house in the NFL (National Football League) in the last quarter, with many favored teams winning. Certainly, the unfavorable payout did not help the big players.

It’s difficult to give definitive answers, but one thing is certain: since then, the two main US bookmakers have announced that they are entering the predictive betting market with their own proprietary platforms.

FanDuel and DraftKings decided to move at that moment.

As I said, event contracts — framed as federally regulated derivatives/contracts — have allowed prediction markets to offer “bets” on sports and events even in states where online sports betting is not legal (California and Texas are among the wealthiest and most populous states). This has created a new competitive front and a jurisdiction war between federal regulation and state authorities.

Initially, prediction market platforms only offered binary options (yes or no, for example), but since 2025, they have introduced multiple options, including for sports, effectively becoming true betting platforms, but unregulated or operating in gray markets, thus having a competitive advantage.

When this step was taken, especially by financial exchanges — as I anticipated — Wall Street reacted negatively and also penalized stocks related to traditional betting, such as Flutter.

Precisely for this reason, the two main US bookmakers, Fanduel (owned by Flutter) and DraftKings, have adapted and are launching their own platforms.

FanDuel has not copied the Polymarket model: it has chosen a hyper-institutional path. At the end of December 2025, FanDuel and CME Group announced the launch of FanDuel Predicts, with an initial rollout in some states, under the umbrella of the federal financial derivatives oversight commission.

In the press release (and in the first public details), the approach is very clear: contracts on financial benchmarks (like stock indices and commodities) and economic indicators, in addition to the “event-based” perimeter. It is a way to:

When FanDuel decided to launch FanDuel Predicts, it didn’t just add a new feature to its app. It did something more subtle, and potentially more disruptive: it tried to shift the cultural boundary between betting and finance. For years, online betting has been presented as entertainment, adrenaline, cheering. Here, however, the grammar changes. You no longer bet on a match: you trade probabilities, buy scenarios, sell expectations. It’s the lexicon of markets, not betting slips. The collaboration with CME Group, the Chicago derivatives giant, is not a technical detail but a political manifesto: it means telling investors and regulators that these contracts resemble simplified futures more than bar bets. And indeed, the regulatory umbrella is not that of state gambling, but that of the federal Commodity Futures Trading Commission, the same authority that oversees commodities and financial markets. Inside FanDuel Predicts, you will find binary markets, yes or no, which can concern the outcome of a match but also the trend of the S&P 500, inflation, the price of oil. It is a silent mutation: the sportsbook becomes a small popular stock exchange, accessible from a smartphone, where the user is not just a fan but a micro-trader. And above all, it is a strategic move to circumvent the fragmented geography of US betting laws: where sports betting is still prohibited, federally regulated event contracts can still pass. Thus, FanDuel not only expands its offering but the very perimeter of the market, intercepting an audience that is not looking for stadium thrills, but for tools to monetize opinions about the world. If prediction markets truly become a new asset class, FanDuel Predicts is the signal that Wall Street and Las Vegas have stopped looking at each other with suspicion and have discreetly started talking to each other.

CME Group is a leading US global derivatives market company, operating major exchanges such as the Chicago Mercantile Exchange (CME), Chicago Board of Trade (CBOT), New York Mercantile Exchange (NYMEX), and COMEX. Through these platforms, it offers trading in futures and options on a wide range of assets — from interest rates and stock indices to currencies, commodities, and energy — enabling institutional investors and traders worldwide to manage risk, hedge positions, and access global benchmarks in financial markets.

DraftKings opted for the intermediary route with its own app. The well-known bookmaker officially entered prediction markets on December 19, 2025 with DraftKings Predictions, explaining that the operation is carried out through a subsidiary registered as an Introducing Broker and NFA member (National Futures Association), and is available in 38 states (including major markets).

For DraftKings, the value is twofold:

It is no coincidence that, as early as 2025, CEO Jason Robins openly spoke about the opportunity in “non-sports-betting states“.

Ultimately, setting aside the dust kicked up by tweets, stock market alarms, and regulatory anxieties, a rather American truth remains: prediction markets make a lot of noise, but little real damage. At least for now.

According to a report released by Citizens Equity Research, prediction markets have diverted about 5% of the regulated gaming volume from traditional bookmakers. Translated into dollars: about $8 billion per year. A figure that seems impressive only until you remember that the handle — the volume of bets — is not revenue, is not margin, is not profit. It’s movement. Like highway traffic: it doesn’t say how much the toll booth earns.

The analysis is signed by Jordan Bender, who immediately gets to the point: that 5% is slightly higher than previously estimated, but it is not an event capable of changing the fundamentals of the sector. No hemorrhage, no systemic business theft.

From the companies’ perspective, says Bender, the impact is a wash, a break-even. DraftKings, FanDuel (and therefore the parent company Flutter Entertainment) are not losing sleep: they are already present, directly or indirectly, in the world of prediction markets. If the game changes form, they change tables.

Some more trouble might come for those who have remained on the sidelines: Bet365, BetMGM, Caesars, Penn Entertainment. But even here, in the analyst’s words, we are talking about “slightly negative” scenarios. Nothing structural, nothing that justifies hysterics.

An exception is Rush Street Interactive: little exposure to prediction markets, excellent stock performance in the last year, and a strategy more focused on iGaming, which offers a certain immunity. On the contrary, paradoxically, the company could even benefit from the phenomenon: if yes/no markets erode the tax revenue from sports betting, they could push more US states to legalize traditional iGaming. The usual America: you lose on one side, you gain on the other.

But if companies manage, players do not. And this is where the story changes tone.

Data shows that retail users of prediction markets burn through money faster than any other form of gambling. In the first 90 days of entering these platforms, the average loss is 7% of bets, compared to 1% recorded in the rest of the online gambling ecosystem.

The reason is simple and cruel: in prediction markets, ordinary players do not compete against the house, but against other players, often much more prepared. “Sharp” bettors — those with models, official data, sophisticated pricing — find an ideal ground here, especially since platforms like Kalshi actively incentivize them.

The damage is amplified by another detail: the average bet. In prediction markets, it exceeds $185, more than triple the average of $55 in regulated sportsbooks. Losing more, more often, and with higher stakes is a lethal combination.

Bender synthesizes it without poetry but effectively: prediction markets are creating worse losses for the worst players, while the more skilled ones win more. Furthermore, the odds are generally worse than traditional bookmakers. Throughout the 2025 NFL season, for example, the prices offered by Kalshi consistently proved less favorable than those of DraftKings and FanDuel.

So why all this panic in the financial markets?

According to the analyst, because the reaction was disproportionate. DraftKings and Flutter stocks lost 33% and 30% respectively from their 52-week highs, but the real impact of prediction markets does not justify such cannibalization even remotely.

To be clear: a single bad Monday Night Football game can have a negative impact on EBITDA equal to — or greater than — everything that prediction markets are currently subtracting from the sector. And in the long run, Bender adds, the expansion of legalized online sports betting will tend to further restrict the space for these alternative markets, simply by offering a better product.

Finally, the map. Not all of America is the same. According to Juice Reel data, Florida, Georgia, and Texas remain on the sidelines of this phenomenon. Leading the way are the usual suspects: New York, New Jersey, California, Washington, and Ohio.

Prediction markets are not the end of bookmakers, nor the beginning of a new golden age. They are a noisy, fascinating, often ruthless experiment for the less equipped. And as always, in the great American casino, the real losers are not those who play the game, but those who think they have understood the rules without ever having read them thoroughly.

In summary:

One thing is evident happening on Wall Street: investors are desperately seeking listed companies that have a connection — even indirect — with this new segment.

The problem concerns the big names in prediction markets, such as Kalshi and Polymarket, which remain private companies. Conversely, some listed companies orbiting the theme, such as Robinhood Markets, are highly diversified financial groups, not platforms dedicated to trading predictive contracts.

The same applies to betting operators like DraftKings and Flutter Entertainment: they are now entering the world of prediction markets, but it is likely that, at least in the short term, this activity will represent only a marginal fraction of their revenues.

In the USA, there is one stock that has caught investors’ attention: High Roller, a company that manages online casinos in Scandinavian markets and is based in Malta.

Investors’ hunger for opportunities in this sector also explains the recent enthusiasm around the High Roller stock. It is not a “pure” prediction market company, but it is one of the few listed companies that allow investors to get close to that world.

When a new idea meets the market, it often happens like this: first euphoria, then selection. The price rises, falls, settles. And in the end, as always, only one question remains: how much of that promise will actually become revenue?

2026 has only completed one month, and the High Roller stock has already given its investors a rollercoaster experience. At the beginning of the year, the price hovered around $2. Then, in a matter of days, the surge: almost $24. Today, the value has halved.

A large part of that rally is concentrated on a single date, January 14, when the stock recorded an incredible +688 percent. That day, High Roller announced a partnership on prediction markets with Crypto.com. From that moment on, many traders began to look at the company not just as a simple online casino operator, but as a possible indirect bet on the world of event contracts.

“We are excited to bring High Roller to the United States through this strategic partnership with Crypto.com,” said CEO Seth Young. “Combining the huge appeal of prediction markets with our distribution capabilities is an extremely exciting opportunity.”

High Roller manages the online casino brands High Roller and Fruta and went public on Wall Street in October 2024, after reducing the size of its initial public offering just a month earlier.

How much of prediction markets will actually enter High Roller’s accounts, and with what margins? Today, no one knows, but the investors’ interest in these stocks remains tangible.

Polymarket is considered one of the leading global prediction markets with a crypto-native approach.

Currency/Asset used:

➡️ USD Coin (USDC), a stablecoin pegged to the US dollar. Users buy and sell contracts using USDC as a deposit and settlement medium, with technical scaffolding on networks like Polygon. After three years of suspension, Polymarket was authorized in 2025 to re-enter the official US market.

Key features:

👉 Polymarket continues to operate with stablecoins (USDC) as the “base currency” for international predictive contracts.

Polymarket obtained, in November 2025, CFTC approval for a regulated return to the US market (U.S. Commodity Futures Trading Commission). It had blocked access to US users in 2022 after a regulatory action and a fine from the CFTC for operating as a derivatives market without registration.

✅ After three years, the CFTC issued an Amended Order of Designation allowing Polymarket to:

Why this step is important

🔹 The approval allows Polymarket to operate under the same regulatory framework as US exchanges (at the federal level, but we will see the problems encountered in individual states)

🔹 US users will be able to access prediction markets through regulated channels (no longer just offshore).

🔹 The platform has already enhanced its compliance, supervision, clearing, and regulatory reporting systems to meet the required standards.

How it got there

➡️ Polymarket acquired QCX LLC, a CFTC-licensed derivatives exchange and clearinghouse, thus providing the legal basis to operate in the US market.

Broader implications

👉 The move signals greater regulatory acceptance of prediction markets in the USA (undoubtedly Trump’s election facilitated this process).

👉 Potential increase in trading volume in the sector compared to the previous situation.

👉 Polymarket’s return contributes to pushing prediction markets into the traditional financial ecosystem.

Next steps

⏳ Before regulated trading becomes fully active, Polymarket must:

Kalshi is a fully regulated predictive contract exchange by the Commodity Futures Trading Commission (CFTC) in the United States, becoming one of the most important compliant infrastructure exchanges for institutional and retail traders.

Kalshi, Inc. is a US prediction market platform founded in 2018 by Tarek Mansour and Luana Lopes Lara, two former financial analysts who met at MIT (Massachusetts Institute of Technology). Today it is headquartered in New York City and is a private company with a market valuation of approximately $11 billion after a $1 billion funding round, with investors including Sequoia Capital, Paradigm, Y Combinator, and asset managers like Charles Schwab and Henry Kravis.

Kalshi is not a normal betting site: its offering is based on “event contracts”, financial contracts that allow users to buy/sell predictions on the outcome of real events — from climate and economic data, to politics, as well as sports and legislative results — with the contract price reflecting the market’s perceived probability. Unlike traditional bookmakers, Kalshi does not bet against the user but acts as an organized market where buyers and sellers meet, and it earns profits through transaction commissions.

The company operates as a regulated exchange in the United States under the authority of the Commodity Futures Trading Commission (CFTC), which in 2020 approved Kalshi as a Designated Contract Market — the first platform of its kind to obtain this federal recognition for predictive markets. This status allows it to offer tradable events, but it also entails legal challenges with individual states (especially when Kalshi began offering markets on sports results), because some state regulators believe that certain contracts constitute actual unauthorized sports betting.

In summary, Kalshi is seeking to redefine the boundary between predictive finance and regulated gaming, attracting both institutional liquidity and the attention of regulators, and positioning itself as a global market infrastructure for trading in advance on the outcome of real events.

The currency used by Kalshi ➡️ USD fiat — the main market is in US dollars.

Kalshi also allows deposits via stablecoins or cryptocurrencies in some cases, but these are automatically converted to USD before absorbing trading contracts.

Fiat currency means, from Latin, both made (by decree). When we talk about fiat currencies, we are talking about traditional currencies like the dollar, euro, yen, ruble, etc.

Key features:

👉 Although Kalshi may accept crypto deposits → USD, its core operation is tied to fiat currency markets, not native tokens or stablecoins as the primary market medium.

| Platform | Main Currency | Features | Typical User Type |

|---|---|---|---|

| Polymarket | USDC (stablecoin) | In transition, under CFTC compliance, decentralized structure | Global traders, crypto-native |

| Kalshi | USD (fiat) | CFTC regulated | Institutional / US retail traders |

| PredictIt | USD | It is a site focused on politics | Political bettors |

| Opinion.Trade | Crypto (e.g., BNB Chain token) | Decentralized | Crypto traders / dApp users |

| Crypto.com Markets | Crypto / stablecoin | Integrated exchange | Crypto Ecosystem |

✔️ The main prediction markets use a combination of currencies:

✔️ In the United States, it’s not that platforms have completely eliminated stablecoins, but Kalshi structures the use of cryptocurrencies as a gateway to convert them into fiat market, while Polymarket is trying to balance the use of stablecoins and regulatory compliance to fully re-enter the US market.

Within a few months, the advance of prediction markets (Kalshi, Polymarket, and the “event contracts” ecosystem) has forced the two giants of US betting — FanDuel (Flutter) and DraftKings — to make a choice: suffer competitors who bypass the state borders of traditional betting, or enter it with a proprietary product.

And the answer, today, is clear: they have entered it.

A stablecoin pegged to the dollar is, in essence, a digital dollar: a cryptocurrency designed to maintain a stable value (1 token = 1 USD) thanks to reserves in cash, government bonds, or liquid instruments held by the issuer. It is used to move money on the blockchain with the speed of crypto trading but with the stability of fiat currency, thus becoming the “cash” of digital markets, from payments to prediction markets. The most common are USDT (Tether), the queen for global volumes, USDC (Circle/Coinbase), perceived as more regulated and transparent in the US, and DAI, decentralized and collateralized on-chain. But their weight goes beyond finance: stablecoins have also become a geopolitical tool, as they effectively export the dollar outside the traditional banking system, allowing millions of people — and sometimes countries under sanctions or with weak currencies — to use “digital USD” without going through SWIFT or central banks. For Washington, it is monetary soft power; for regulators, it is also a systemic risk and a control issue: too many dollars circulating outside the banking perimeter mean fewer levers on capital, sanctions, and monetary policy. In short: fintech technology on the surface, but a struggle for economic sovereignty flows underneath.

The question on the minds of many keen observers is: “Are traditional bookmakers just watching while platforms operating (in most cases in markets not yet regulated) ‘eat up’ market share?”

In October 2025, the stock market crash of Flutter (owner of the leading US bookmaker Fanduel) and DraftKings sounded like an alarm bell.

Some stock market analysts were quick to draw a connection between the financial markets’ reaction and the new competition from Polymarket and its peers in sports.

There is also a significant detail, given that the decisive battle for the future of global betting is being fought in the USA (with substantial investments and strong “bets” and investments from Wall Street).

In important states (like California), betting is not legally permitted, but with the loophole of “financial” derivative contracts (recognized at the federal level), Polymarket and Kalshi are effectively collecting bets where no other betting operator is allowed. In the long run, this gap risks becoming insurmountable.

Other observers, however, attributed the causes to the negative results recorded by the house in the NFL (National Football League) in the last quarter, with many favored teams winning. Certainly, the unfavorable payout did not help the big players.

It’s difficult to give definitive answers, but one thing is certain: since then, the two main US bookmakers have announced that they are entering the predictive betting market with their own proprietary platforms.

FanDuel and DraftKings decided to move at that moment.

As I said, event contracts — framed as federally regulated derivatives/contracts — have allowed prediction markets to offer “bets” on sports and events even in states where online sports betting is not legal (California and Texas are among the wealthiest and most populous states). This has created a new competitive front and a jurisdiction war between federal regulation and state authorities.

Initially, prediction market platforms only offered binary options (yes or no, for example), but since 2025, they have introduced multiple options, including for sports, effectively becoming true betting platforms, but unregulated or operating in gray markets, thus having a competitive advantage.

When this step was taken, especially by financial exchanges — as I anticipated — Wall Street reacted negatively and also penalized stocks related to traditional betting, such as Flutter.

Precisely for this reason, the two main US bookmakers, Fanduel (owned by Flutter) and DraftKings, have adapted and are launching their own platforms.

FanDuel has not copied the Polymarket model: it has chosen a hyper-institutional path. At the end of December 2025, FanDuel and CME Group announced the launch of FanDuel Predicts, with an initial rollout in some states, under the umbrella of the federal financial derivatives oversight commission.

In the press release (and in the first public details), the approach is very clear: contracts on financial benchmarks (like stock indices and commodities) and economic indicators, in addition to the “event-based” perimeter. It is a way to:

When FanDuel decided to launch FanDuel Predicts, it didn’t just add a new feature to its app. It did something more subtle, and potentially more disruptive: it tried to shift the cultural boundary between betting and finance. For years, online betting has been presented as entertainment, adrenaline, cheering. Here, however, the grammar changes. You no longer bet on a match: you trade probabilities, buy scenarios, sell expectations. It’s the lexicon of markets, not betting slips. The collaboration with CME Group, the Chicago derivatives giant, is not a technical detail but a political manifesto: it means telling investors and regulators that these contracts resemble simplified futures more than bar bets. And indeed, the regulatory umbrella is not that of state gambling, but that of the federal Commodity Futures Trading Commission, the same authority that oversees commodities and financial markets. Inside FanDuel Predicts, you will find binary markets, yes or no, which can concern the outcome of a match but also the trend of the S&P 500, inflation, the price of oil. It is a silent mutation: the sportsbook becomes a small popular stock exchange, accessible from a smartphone, where the user is not just a fan but a micro-trader. And above all, it is a strategic move to circumvent the fragmented geography of US betting laws: where sports betting is still prohibited, federally regulated event contracts can still pass. Thus, FanDuel not only expands its offering but the very perimeter of the market, intercepting an audience that is not looking for stadium thrills, but for tools to monetize opinions about the world. If prediction markets truly become a new asset class, FanDuel Predicts is the signal that Wall Street and Las Vegas have stopped looking at each other with suspicion and have discreetly started talking to each other.

CME Group is a leading US global derivatives market company, operating major exchanges such as the Chicago Mercantile Exchange (CME), Chicago Board of Trade (CBOT), New York Mercantile Exchange (NYMEX), and COMEX. Through these platforms, it offers trading in futures and options on a wide range of assets — from interest rates and stock indices to currencies, commodities, and energy — enabling institutional investors and traders worldwide to manage risk, hedge positions, and access global benchmarks in financial markets.

DraftKings opted for the intermediary route with its own app. The well-known bookmaker officially entered prediction markets on December 19, 2025 with DraftKings Predictions, explaining that the operation is carried out through a subsidiary registered as an Introducing Broker and NFA member (National Futures Association), and is available in 38 states (including major markets).

For DraftKings, the value is twofold:

It is no coincidence that, as early as 2025, CEO Jason Robins openly spoke about the opportunity in “non-sports-betting states“.

Ultimately, setting aside the dust kicked up by tweets, stock market alarms, and regulatory anxieties, a rather American truth remains: prediction markets make a lot of noise, but little real damage. At least for now.

According to a report released by Citizens Equity Research, prediction markets have diverted about 5% of the regulated gaming volume from traditional bookmakers. Translated into dollars: about $8 billion per year. A figure that seems impressive only until you remember that the handle — the volume of bets — is not revenue, is not margin, is not profit. It’s movement. Like highway traffic: it doesn’t say how much the toll booth earns.

The analysis is signed by Jordan Bender, who immediately gets to the point: that 5% is slightly higher than previously estimated, but it is not an event capable of changing the fundamentals of the sector. No hemorrhage, no systemic business theft.

From the companies’ perspective, says Bender, the impact is a wash, a break-even. DraftKings, FanDuel (and therefore the parent company Flutter Entertainment) are not losing sleep: they are already present, directly or indirectly, in the world of prediction markets. If the game changes form, they change tables.

Some more trouble might come for those who have remained on the sidelines: Bet365, BetMGM, Caesars, Penn Entertainment. But even here, in the analyst’s words, we are talking about “slightly negative” scenarios. Nothing structural, nothing that justifies hysterics.

An exception is Rush Street Interactive: little exposure to prediction markets, excellent stock performance in the last year, and a strategy more focused on iGaming, which offers a certain immunity. On the contrary, paradoxically, the company could even benefit from the phenomenon: if yes/no markets erode the tax revenue from sports betting, they could push more US states to legalize traditional iGaming. The usual America: you lose on one side, you gain on the other.

But if companies manage, players do not. And this is where the story changes tone.

Data shows that retail users of prediction markets burn through money faster than any other form of gambling. In the first 90 days of entering these platforms, the average loss is 7% of bets, compared to 1% recorded in the rest of the online gambling ecosystem.

The reason is simple and cruel: in prediction markets, ordinary players do not compete against the house, but against other players, often much more prepared. “Sharp” bettors — those with models, official data, sophisticated pricing — find an ideal ground here, especially since platforms like Kalshi actively incentivize them.

The damage is amplified by another detail: the average bet. In prediction markets, it exceeds $185, more than triple the average of $55 in regulated sportsbooks. Losing more, more often, and with higher stakes is a lethal combination.

Bender synthesizes it without poetry but effectively: prediction markets are creating worse losses for the worst players, while the more skilled ones win more. Furthermore, the odds are generally worse than traditional bookmakers. Throughout the 2025 NFL season, for example, the prices offered by Kalshi consistently proved less favorable than those of DraftKings and FanDuel.

So why all this panic in the financial markets?

According to the analyst, because the reaction was disproportionate. DraftKings and Flutter stocks lost 33% and 30% respectively from their 52-week highs, but the real impact of prediction markets does not justify such cannibalization even remotely.

To be clear: a single bad Monday Night Football game can have a negative impact on EBITDA equal to — or greater than — everything that prediction markets are currently subtracting from the sector. And in the long run, Bender adds, the expansion of legalized online sports betting will tend to further restrict the space for these alternative markets, simply by offering a better product.

Finally, the map. Not all of America is the same. According to Juice Reel data, Florida, Georgia, and Texas remain on the sidelines of this phenomenon. Leading the way are the usual suspects: New York, New Jersey, California, Washington, and Ohio.

Prediction markets are not the end of bookmakers, nor the beginning of a new golden age. They are a noisy, fascinating, often ruthless experiment for the less equipped. And as always, in the great American casino, the real losers are not those who play the game, but those who think they have understood the rules without ever having read them thoroughly.

In summary:

One thing is evident happening on Wall Street: investors are desperately seeking listed companies that have a connection — even indirect — with this new segment.

The problem concerns the big names in prediction markets, such as Kalshi and Polymarket, which remain private companies. Conversely, some listed companies orbiting the theme, such as Robinhood Markets, are highly diversified financial groups, not platforms dedicated to trading predictive contracts.

The same applies to betting operators like DraftKings and Flutter Entertainment: they are now entering the world of prediction markets, but it is likely that, at least in the short term, this activity will represent only a marginal fraction of their revenues.

In the USA, there is one stock that has caught investors’ attention: High Roller, a company that manages online casinos in Scandinavian markets and is based in Malta.

Investors’ hunger for opportunities in this sector also explains the recent enthusiasm around the High Roller stock. It is not a “pure” prediction market company, but it is one of the few listed companies that allow investors to get close to that world.

When a new idea meets the market, it often happens like this: first euphoria, then selection. The price rises, falls, settles. And in the end, as always, only one question remains: how much of that promise will actually become revenue?

2026 has only completed one month, and the High Roller stock has already given its investors a rollercoaster experience. At the beginning of the year, the price hovered around $2. Then, in a matter of days, the surge: almost $24. Today, the value has halved.

A large part of that rally is concentrated on a single date, January 14, when the stock recorded an incredible +688 percent. That day, High Roller announced a partnership on prediction markets with Crypto.com. From that moment on, many traders began to look at the company not just as a simple online casino operator, but as a possible indirect bet on the world of event contracts.

“We are excited to bring High Roller to the United States through this strategic partnership with Crypto.com,” said CEO Seth Young. “Combining the huge appeal of prediction markets with our distribution capabilities is an extremely exciting opportunity.”

High Roller manages the online casino brands High Roller and Fruta and went public on Wall Street in October 2024, after reducing the size of its initial public offering just a month earlier.

How much of prediction markets will actually enter High Roller’s accounts, and with what margins? Today, no one knows, but the investors’ interest in these stocks remains tangible.

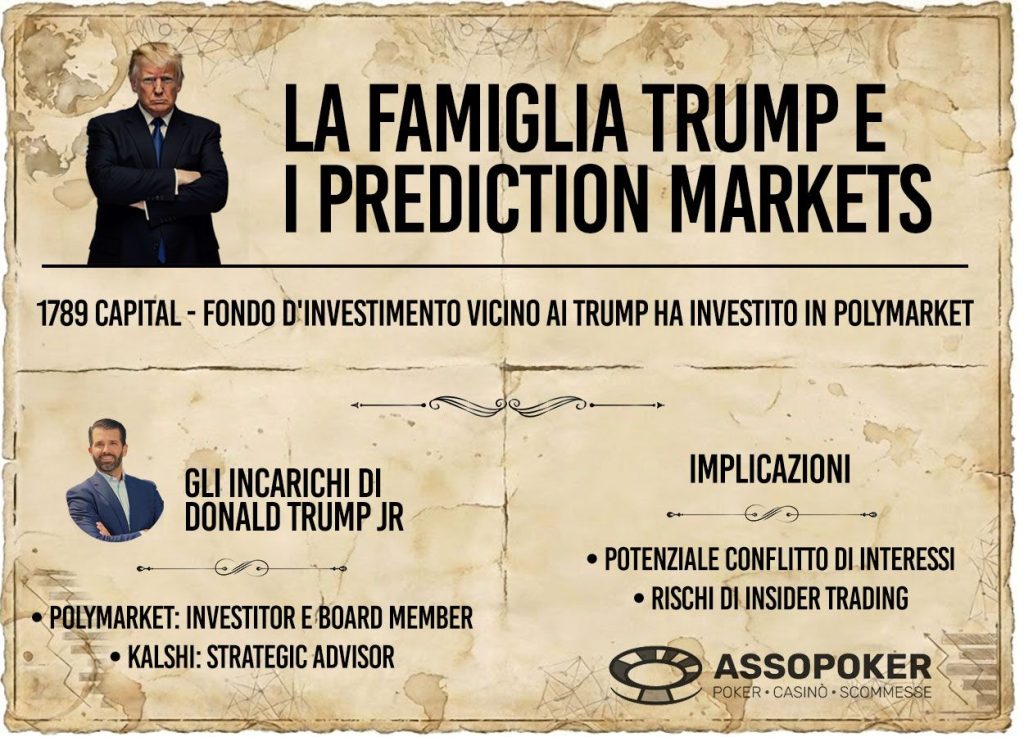

📍 1789 Capital and prediction markets

🚀 Investment in Polymarket:

1789 Capital made a multi-million dollar investment in Polymarket (in the order of “double-digit millions“, i.e., tens of millions), one of the world’s leading prediction markets, and at the same time Donald Trump Jr. joined the company’s advisory board.

📈 Role in Kalshi:

In parallel, Trump Jr. was appointed strategic advisor of Kalshi, the main competitor platform to Polymarket in the United States, although there is no direct investment from the 1789 Capital fund in Kalshi (at least according to publicly available information).

💡 Therefore, the link with both major operators of prediction markets — Polymarket and Kalshi — passes mainly through Donald Trump Jr. and his position in 1789 Capital, which invested in Polymarket and brought Trump Jr. as a key figure also to Kalshi.

📌 Why it is relevant

This link between a fund connected to the Trump family and the main prediction market operators has attracted attention for several reasons:

Prediction markets, due to the subject of their bets, open up an enormous potential risk for insider trading incidents. One of the most striking examples occurred with the arrest (for some observers, it is actually the kidnapping of a head of state) of Venezuelan President Nicolas Maduro.

On Polymarket, some accounts began betting on the blitz and arrest of Maduro a few hours before the secret operation by US special forces in the South American country began.

The fact is that, since the market on the potential capture of the Venezuelan president by January 31 was opened, the probabilities provided were very low. The event was judged improbable. But a few hours before the US special forces’ raid in Caracas, on Polymarket, the probabilities suddenly moved, and the event — quite suddenly and “unexpectedly” — became increasingly likely, while on other platforms everything remained unchanged.

The numbers speak for themselves and “predict” the future: an account created just a few hours earlier invested $30,000 and cashed out over $436,000. Not a stroke of luck, but seemingly a surgical operation, timed with a disquieting precision by some well-informed source. The witch hunt has also begun: some pointed fingers at officials close to Trump, while exponents close to the US administration accused Venezuelan insiders (did they know beforehand?).

That insider trading is one of the dangers of predictive betting markets is like discovering hot water, but after this episode, the red light has flashed.

One of the revealing details is the comparison with competing platforms like Kalshi, where probabilities remained low until the last moment, almost indifferent to the impending earthquake.

Two markets, two readings of reality. And an inevitable question: who knew what, and when?

It should also be noted: Kalshi treats the exchange of user predictions as financial instruments and is under the supervision of a federal agency, the Commodity Futures Trading Commission (CFTC), which oversees derivatives (as predictive markets are also treated by some states in the USA). Therefore, it is much more difficult to carry out operations that could arouse suspicion. The real risk is ending up in jail.

Polymarket is still in a regulatory limbo. At the moment, it operates in a sort of unregulated market, but it is close to federal commission CFTC supervision.

Among traders, opaque practices by some users are known: from “wash trading” to artificially inflate volumes, to suspiciously accurate bets on technological events, corporate decisions, and even updates to platform algorithms and search engines. Each time, the same shadow: the use of confidential information by some accounts, given that there is the problem — on most of these platforms — of anonymous accounts.

The Maduro case, however, raises the stakes. Here we are not talking about quarterly profits or product launches, but about a militarily explosive geopolitical operation and arrest that few knew about. This is the point where the market stops being a thermometer and risks becoming an insider club.

It is no coincidence that Democratic Representative Ritchie Torres has announced a new legislative proposal, the Public Integrity in Financial Prediction Markets Act of 2026, aimed at prohibiting or limiting the participation of public officials and political figures in these markets. The principle is simple: those with access to power should not be able to monetize advance knowledge of their decisions.

Prediction markets were born as transparency tools, capable — at least in theory — of predicting the future better than polls and traditional intelligence. But when the future becomes a source of income for a well-informed few, the line between prediction and manipulation becomes dangerously thin. And at that point, it is democracy, more than the market, that demands guarantees.

As we have seen, prediction markets (predictive markets) are markets where users buy and sell financial contracts that pay out based on the outcome of real events — such as political elections, economic results, sports, etc. — with the aim of translating the implicit probability of an event into prices. Let’s discover the main players, the most important platforms.

Polymarket — as you have gathered — is the American prediction market platform based on blockchain technology, founded in 2020 by Shayne Coplan with headquarters in New York City. Unlike traditional online bookmakers, Polymarket offers a decentralized prediction market where users can buy and sell shares (“shares”) related to the outcome of future events — from politics and the real economy, to sports, weather, and pop culture — using stablecoins (USDC) on the Polygon network, a scaling layer of Ethereum.

Polymarket’s operational structure is inherently decentralized and crypto-native, with transactions on the markets occurring on-chain and share prices reflecting the implicit probability of outcomes based on the “wisdom of crowds”. Users buy “Yes” or “No” positions, and if the outcome is correct, each share resolves to $1 USDC, while incorrect ones expire at zero — a mechanism similar to a binary contract that serves as a real-time probability signal.

Polymarket has attracted significant institutional investment, including a deal with Intercontinental Exchange (ICE) — owner of the New York Stock Exchange — which brought a commitment of up to $2 billion, valuing the platform at around $8 billion and marking one of the largest endorsements from a traditional financial institution in the prediction market sector.

Regulators and markets, however, have represented a complex terrain: after an initial agreement with the CFTC in 2022 that limited access for US users due to registration issues, Polymarket has taken steps towards regulatory compliance by acquiring a licensed derivatives exchange (QCEX) to fully re-enter the US market and expand its reach into regulated markets.

In summary, Polymarket positions itself as the world’s largest blockchain-based prediction market, combining Web3 technology, crypto liquidity, and collective market signals to transform future events into tradable assets, but always operating on the edge between financial innovation and global regulatory complexity.

The currency that holds everything together is USD Coin (USDC), a stablecoin pegged to the US dollar. It is the silent fuel of the platform: deposit, medium of exchange, and settlement instrument. Every contract goes through it, as if it were a digital dollar flowing faster and without intermediaries. The technical infrastructure relies on networks like Polygon, chosen for its low costs and execution speed: fundamental characteristics when the market needs to react in real time to breaking news or election results.

Everything works through smart contracts. No discretion, no cash. If the event occurs, payment is automatic. A binary logic, almost mathematical: yes or no. 1 or 0. It is this simplicity that makes Polymarket global and immediate, capable of attracting users from all over the world, even if not all jurisdictions look upon it favorably. Some countries and several US states, as well as stricter regulatory markets like France, the UK, or Singapore, limit or block direct access, reminding us that the line between financial prediction and betting remains politically very sensitive.

The real breakthrough, however, is not technological. It is regulatory, as we have just mentioned. In 2022, Polymarket had to close its doors to US users after an intervention by the Commodity Futures Trading Commission, which contested its operation without registration. Fine, forced stop, exit from the richest market in the world. For a platform born in the USA, it was almost an exile.

Politics in the USA influences everything, even business and justice. The President has — among his powers — significant influence (with ad hoc appointments) over the federal Attorneys General of the Department of Justice, and under the Biden administration, Polymarket did not fare well. In 2024, an FBI raid under a warrant from the DOJ itself destabilized the company.

Fortunately for the platform, in July 2025, the Department of Justice (DOJ) and the Commodity Futures Trading Commission (CFTC) officially closed the civil and criminal investigations into the company without proceeding with further charges.

The investigations were initiated after Polymarket received a visit from the FBI in 2024 and underwent searches for suspected continued acceptance of bets from US users, despite the previous agreement with the CFTC in 2022 which had required it to cease operations in the USA and pay a $1.4 million fine for operating as a derivatives market without registration.

The core of the accusation was that Polymarket had violated that agreement by continuing to access the US market — a potential infraction both civilly and criminally.

With the Trump administration, the wind changed. In the summer of 2025, both the DOJ and the CFTC notified Polymarket of the closure of their respective investigations and the decision not to file further charges. This was a significant turn of events, especially considering that one of the investigations also included a criminal component.

The authorities did not release details on the outcome of the investigations or the specific reasons for the decision, but the epilogue marked the end of months of regulatory uncertainty for the company.

The closure of the investigations came at a time of strong growth for the platform and regulatory change in the prediction market sector.

Not long after, Polymarket concluded the acquisition of the US derivatives exchange and clearinghouse QCX for approximately $112 million — a fundamental strategic move to re-enter the US market in compliance with CFTC regulations.

In fact, Polymarket not only avoided criminal or civil charges but is now on the path to re-establishing its presence in the USA in a more rigorous and formally approved regulatory context.

Three years later, the return. In November 2025, the CFTC granted Polymarket formal approval, an Amended Order of Designation that allows it to re-enter the United States as a regulated operator. No longer a gray area, no longer offshore. But the same legal perimeter as US derivatives exchanges. In practice, Polymarket can operate as a true exchange, offering trading to US users through authorized intermediaries, traditional brokers, and futures commission merchants. In 2026, Polymarket is in a due diligence phase in the USA.

This is a step that changes perception even more than numbers. Because it means institutional legitimacy.

To get there, the company chose a strategic shortcut: the acquisition — as we recalled — of QCX LLC, an exchange and clearinghouse already holding a CFTC license. By buying the regulated infrastructure, Polymarket also bought the legal basis to operate in the United States. A textbook finance operation, rather than a crypto startup.

Since then, the project has changed its skin. Strengthened compliance systems, internal supervision, clearing, regulatory reporting: everything needed to speak the language of federal authorities. The goal is clear: to transform a market born on the fringes into an infrastructure capable of dialoguing with Wall Street.

The implications go beyond the single company. Polymarket’s return signals growing acceptance of prediction markets by US regulators and suggests a possible increase in the sector’s overall liquidity. More legal certainty, less reputational risk, more institutional capital. In other words: more volumes.

Now, the final stretch remains, the operational one. Before regulated trading is fully active, Polymarket will have to complete integration with US intermediaries and define precise procedures for mediated user access. But the direction is set.

From a frontier platform to a recognized financial infrastructure.

And for a market that sells probabilities about the future, it is perhaps the most important prediction of all.

Polymarket is considered one of the leading global prediction markets with a crypto-native approach.

Currency/Asset used:

➡️ USD Coin (USDC), a stablecoin pegged to the US dollar. Users buy and sell contracts using USDC as a deposit and settlement medium, with technical scaffolding on networks like Polygon. After three years of suspension, Polymarket was authorized in 2025 to re-enter the official US market.

Key features:

👉 Polymarket continues to operate with stablecoins (USDC) as the “base currency” for international predictive contracts.

Polymarket obtained, in November 2025, CFTC approval for a regulated return to the US market (U.S. Commodity Futures Trading Commission). It had blocked access to US users in 2022 after a regulatory action and a fine from the CFTC for operating as a derivatives market without registration.

✅ After three years, the CFTC issued an Amended Order of Designation allowing Polymarket to:

Why this step is important

🔹 The approval allows Polymarket to operate under the same regulatory framework as US exchanges (at the federal level, but we will see the problems encountered in individual states)

🔹 US users will be able to access prediction markets through regulated channels (no longer just offshore).

🔹 The platform has already enhanced its compliance, supervision, clearing, and regulatory reporting systems to meet the required standards.

How it got there

➡️ Polymarket acquired QCX LLC, a CFTC-licensed derivatives exchange and clearinghouse, thus providing the legal basis to operate in the US market.

Broader implications

👉 The move signals greater regulatory acceptance of prediction markets in the USA (undoubtedly Trump’s election facilitated this process).

👉 Potential increase in trading volume in the sector compared to the previous situation.

👉 Polymarket’s return contributes to pushing prediction markets into the traditional financial ecosystem.

Next steps

⏳ Before regulated trading becomes fully active, Polymarket must:

Kalshi is a fully regulated predictive contract exchange by the Commodity Futures Trading Commission (CFTC) in the United States, becoming one of the most important compliant infrastructure exchanges for institutional and retail traders.

Kalshi, Inc. is a US prediction market platform founded in 2018 by Tarek Mansour and Luana Lopes Lara, two former financial analysts who met at MIT (Massachusetts Institute of Technology). Today it is headquartered in New York City and is a private company with a market valuation of approximately $11 billion after a $1 billion funding round, with investors including Sequoia Capital, Paradigm, Y Combinator, and asset managers like Charles Schwab and Henry Kravis.

Kalshi is not a normal betting site: its offering is based on “event contracts”, financial contracts that allow users to buy/sell predictions on the outcome of real events — from climate and economic data, to politics, as well as sports and legislative results — with the contract price reflecting the market’s perceived probability. Unlike traditional bookmakers, Kalshi does not bet against the user but acts as an organized market where buyers and sellers meet, and it earns profits through transaction commissions.

The company operates as a regulated exchange in the United States under the authority of the Commodity Futures Trading Commission (CFTC), which in 2020 approved Kalshi as a Designated Contract Market — the first platform of its kind to obtain this federal recognition for predictive markets. This status allows it to offer tradable events, but it also entails legal challenges with individual states (especially when Kalshi began offering markets on sports results), because some state regulators believe that certain contracts constitute actual unauthorized sports betting.

In summary, Kalshi is seeking to redefine the boundary between predictive finance and regulated gaming, attracting both institutional liquidity and the attention of regulators, and positioning itself as a global market infrastructure for trading in advance on the outcome of real events.

The currency used by Kalshi ➡️ USD fiat — the main market is in US dollars.

Kalshi also allows deposits via stablecoins or cryptocurrencies in some cases, but these are automatically converted to USD before absorbing trading contracts.

Fiat currency means, from Latin, both made (by decree). When we talk about fiat currencies, we are talking about traditional currencies like the dollar, euro, yen, ruble, etc.

Key features:

👉 Although Kalshi may accept crypto deposits → USD, its core operation is tied to fiat currency markets, not native tokens or stablecoins as the primary market medium.

| Platform | Main Currency | Features | Typical User Type |

|---|---|---|---|

| Polymarket | USDC (stablecoin) | In transition, under CFTC compliance, decentralized structure | Global traders, crypto-native |

| Kalshi | USD (fiat) | CFTC regulated | Institutional / US retail traders |

| PredictIt | USD | It is a site focused on politics | Political bettors |

| Opinion.Trade | Crypto (e.g., BNB Chain token) | Decentralized | Crypto traders / dApp users |

| Crypto.com Markets | Crypto / stablecoin | Integrated exchange | Crypto Ecosystem |

✔️ The main prediction markets use a combination of currencies: